Restrictions on trade in critical minerals: towards global geoeconomic fragmentation

This document is a copy of the original published by the Spanish Institute for Strategic Studies at the following link.

- Introduction

- Export restrictions and geo-economic fragmentation

- Restrictions and nationalism in critical minerals trade

- Consequences of restrictions

- Conclusions

One of the biggest risks facing trade in these critical minerals is the disruption of supply chains. The high concentration of their production and processing is an extra vulnerability for those powers that depend on external supply such as the US, the EU or Japan.

China, the world's leading producer and export source of many of these minerals, has already shown its willingness to impose export controls on national security grounds. Under cover of this justification, the growing geopolitical tension between China and the US is distorting markets for these minerals. Fragmentation of chains together with the rise of national and regional protectionist measures are some of the risks to the critical minerals economy.

Introduction

Critical minerals (also known as new economy or strategic minerals) are metallic or non- metallic elements that are essential for energy transition, technological progress and di- gitalisation. Some of them are essential for the defence and aerospace sectors.

Criticality is provided not only by the mismatch between supply and demand in terms of onshore geological reserves, but also in terms of the capacity to extract and process them and potential disruptions to supply chains.

Trade in these minerals poses major challenges not only from an economic but also from a security point of view. As we move towards energy transition and technological pro- gress, it is estimated that global demand for these critical minerals may increase by 400- 600% in the coming decades. For lithium and graphite, both used in electric vehicle bat- teries, demand may increase by as much as 4000%1 .

This high demand for critical minerals may become a bottleneck to realising decarbonisa- tion. Today's supply and investment plans for many of these critical minerals fall far short of what would be needed to support the accelerated development of solar panels, wind turbines and electric vehicles to meet climate targets2 . Digital technologies are also con- ditioned by the supply of several elements such as copper, gallium, germanium, gold, indium, rare earths, tantalum and platinum group metals3 .

In addition to this growing demand associated with climate policies, some critical minerals have also become of increasing concern from the point of view of national security and economic growth, mainly for the major powers4 .

One of the greatest risks facing trade in these critical minerals is the disruption of supply chains. The high concentration of production and processing is an extreme vulnerability for powers dependent on external supply such as the US, the EU and Japan.

China, the world's leading producer and export source of many of these minerals, has already shown its willingness to impose export controls on national security grounds. Under cover of this justification, the growing geopolitical tension between China and the US is distorting markets for these minerals. Fragmentation of chains and the rise of national and regional protectionist measures are some of the risks to the critical minerals economy.

Export restrictions and geo-economic fragmentation

The covid-19 pandemic, the war in Ukraine, the food security crisis, geopolitical tensions and dependencies in the energy and digital sectors have highlighted the vulnerability of supply chains in all sectors.

Over the past few years the geopolitical rivalries generated by the war in Ukraine and the growing rivalry between China and the US have fuelled increased protectionism and the growing use of cross-border restrictions on critical raw materials for national security reasons. These restrictions affect energy security, food security, trade in strategic minerals and the entire global economic system.

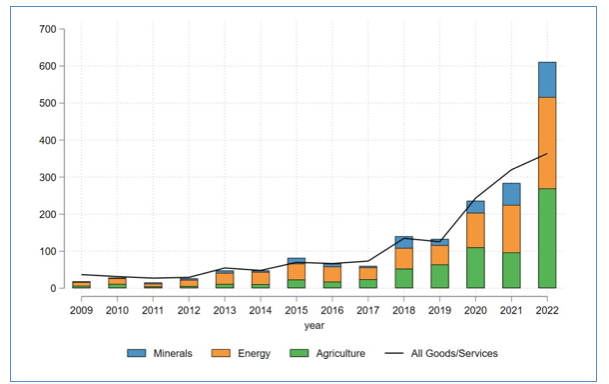

The pace of trade restrictions on critical commodities around the world has increased since 20205 . The number of trade barriers put in place per year has nearly tripled since 2019, according to the IMF, and these protectionist measures continue to affect global trade by limiting volumes traded, increasing costs for companies and hindering supply chains6 . This growing trend of export restrictions on critical materials has triggered a number of trade disputes, some of which are being addressed at the World Trade Organization (WTO)7 .

As Kristalina Georgieva, Managing Director of the International Monetary Fund, states: "The period of rapid globalisation and integration has come to an end, and the forces of protectionism are on the rise. International cooperation is in retreat8 and the world is witnessing increasing fragmentation: a process that begins with rising barriers to trade and investment and, in its extreme form, ends with countries breaking up into rival economic blocs, an outcome that risks reversing the transformative gains that global economic integration has produced"9 . This transformation could lead to a 7% reduction in global economic output10 .

In this context some analysts have coined the term "geo-economic fragmentation"11 to describe a reversal of global economic integration driven by policies generally based on strategic considerations. These considerations might include national or economic security, as well as the enhancement of autonomy through reduced dependence on other countries.

According to the OECD, around 10% of the global value of critical commodity exports have faced at least some export restriction measure in recent years12 . Export restrictions take multiple forms, including quotas, export taxes, compulsory minimum export prices or licensing.

Restrictions and nationalism in critical minerals trade

In the case of critical minerals needed for the energy transition, these restrictions, in addition to contributing to geo-economic fragmentation, put the achievement of climate targets at risk. These measures could affect the global supply of critical minerals, putting upward pressure on world prices and raising concerns about the security of supply of raw materials to manufacturers.

In the specific case of critical minerals used in the renewable energy and technology sectors, their extraction and processing is highly concentrated in a few countries. On the extraction side, for example, the Democratic Republic of Congo accounts for 70% of the world's cobalt mining13 . For nickel, the three main producers (Indonesia, the Philippines and Russia) account for 60% of world production14 . For lithium, the top three producers (Australia, Chile and China) account for more than 90 %15 .

China supplies 80 % of rare earths, refines 68 % of the world's nickel, 40 % of its copper and 59 % of its lithium16 . Chinese companies own 15 of the DRC's 17 cobalt mining operations17 . In addition, it owns 78% of the world's electric vehicle battery manufacturing capacity, most of the world's solar panel production and more than three-quarters of the world's lithium-ion battery factories. China's share of refining is around 35% for nickel, 50% to 70% for lithium and cobalt, and almost 90% for rare earths18 . In fact, there are only five rare earth refineries outside Chinese territory: Nevada, Malaysia, France, Estonia and Australia19.

According to the European Union's Critical Raw Materials 2023 report20 , China is the world's sole supplier of dysprosium (100 %), neodymium (100 %) and yttrium (100 %). It also dominates the supply chain for germanium (83%), gallium (94%) and natural graphite (67%) which are critical in the defence sector, particularly for fighter aircraft, but also for missiles or radar.

In both the EU and the US, there is concern about high dependence on China, or other countries that dominate supply chains for critical minerals, as there is a risk that they may be unable or unwilling to supply these materials in the future. With deepening geopolitical tensions, national security considerations for export restrictions or increased protectionism by states are a barrier to companies' reluctance to invest, share technology or integrate supply chains21 .

In addition to the production of certain critical minerals, China also dominates the processing and manufacturing of components needed for the energy and digital transition. China, aware of this great advantage, has used trade in certain critical minerals as a tool of economic coercion. It already did so with Japan in 2010 following territorial disputes in the South China Sea and restrictions on exports of rare earths on environmental grounds also established in 2010 that were challenged by the US, the EU and Japan at the WTO.

During 2023, China has implemented new restrictions on exports of strategic minerals and associated technology, citing national security concerns. In July it introduced restrictions on export permits for gallium and germanium chip-making materials. On 1 December it established similar requirements for various types of graphite22 and since 21 December it has also extended export restrictions related to the extraction and separation of rare earth technologies to include magnet technology as well.

Gallium and germanium are elements used in the manufacture of microchips used in missile systems and military technology. China accounts for about 94% of the world's gallium and 83% of the world's germanium and currently provides half of US supplies.

Some analysts have viewed gallium and germanium as chess pieces in a geopolitical game of enormous proportions23 . In fact, a 2022 analysis by experts at the US Geological Survey (USGS) found that a 30 percent supply disruption of gallium could cause a $602 billion decrease in US economic output. This would amount to a 2.1 percent reduction in gross domestic product (GDP)24 .

According to a July 2023 report by the Center for Strategic and International Studies entitled Mineral Monopoly: China's Control of Gallium is a National Security Threat, gallium-based semiconductors are crucial for next-generation radar and missile defence systems, electronic warfare and communications equipment25 .

From an extraction point of view, gallium is found in small quantities along with other globally distributed minerals, so it is feasible that other countries could diversify extraction. Gallium is extracted almost exclusively as a by-product of zinc, aluminium and other metal mining26 . The main producers are China, Germany, Kazakhstan and Ukraine27 . However, as with other critical minerals, China dominates the ability to transform and manufacture the ore into useful products for industry and this dependence is more difficult to break in the short term28.

Germanium was one of the first materials used in the production of semiconductors before the widespread use of silicon. It exhibits similar properties to silicon and is used in the production of transistors, diodes and other electronic components29 .

Germanium is extracted as a by-product of zinc production and from coal fly ash. It is estimated that 75 % of the world's germanium production comes from zinc ores, mainly zinc sulphide ore sphalerite, and 25 % from coal30 .

The largest end-use of germanium is in optical fibres, which accounted for 34% of the global germanium consumption volume in 202331 . They are also used in infrared spectroscopes as both germanium and germanium oxide are transparent to infrared radiation. For this reason, it is used to make lenses and windows for IR radiation. These are mainly used in military applications, such as night vision devices. Uses outside the military are in advanced firefighting equipment, satellite imaging sensors and medical diagnostics32 .

According to the European business organisation Critical Raw Materials Alliance (CRMA), China produces about 60 % of the world's germanium, with the remaining 40 % coming from Canada, Finland, Russia and the United States33 .

China dominates the production of these two metals not because they are rare, but because it has been able to keep its production costs fairly low and manufacturers elsewhere have not been able to match them.

Graphite is a material used in batteries, fuel cells and nuclear reactors. China's controls have been justified on "national security" grounds and will require special export permits for three grades of graphite. In 2021, China produced 79.1% of the world's natural graphite, despite having only 22% of the world's reserves34 .

While China argues that these restrictions are in the interests of its national security, some experts point out that it is a move in retaliation to the restrictions on the high-tech sector previously imposed by the US, Japan and the Netherlands by jointly restricting exports of equipment used for the production of the most advanced nodes that can manufacture next-generation chips in response to Chinese President Xi Jinping's "military-civilian fusion" policy 3536 .

China is likely to continue to use its monopoly on the supply of critical materials by imposing new trade restrictions. While it is unlikely that Western countries will be able to completely disengage from China's supply of critical materials in the next 15 years - the estimated time it will take to commission a new mining facility - dependence is likely to decrease over time due to ongoing policy efforts to make supply chains more diversified and to source minerals through recycling.

Consequences of restrictions

One of the first consequences of the latest restrictions imposed by China has been price increases. In particular, gallium prices have already risen significantly by about 30% since the new controls were announced on 3 July, and will continue to rise37 . Prior to the imposition of the restrictions, China had exported 5.1 tonnes of gallium and 8 tonnes of germanium in July38 . However, during August, China sold neither gallium nor germanium on international markets and although Chinese exports of gallium and germanium products rebounded in October, volumes remain well below year ago levels due to the export restrictions introduced in August39 .

The imposition of export restrictions or their sudden removal can also lead to price shocks in the world that directly affect investments in the mining industry, which are necessary for the long term and require large amounts of capital and know-how40 .

China - which remains heavily dependent on the US dollar to set prices and settle commodity contracts - is keen to seize the opportunity presented by the energy transition and its dominance over critical minerals to realise it and increase the renminbi's influence in global commodity markets. To this end, it has established mineral commodity exchanges in resource-rich areas such as the Baotou Rare Earth Commodity Exchange, which became operational in 2014, and the Ganzhou Rare Metal Exchange, where China's renminbi currency is used to quote prices for spot trading of tungsten, rare earth commodities and critical minerals such as cobalt, which as discussed above are essential for the clean energy transition41 .

The search for alternative sources of supply has already become a necessity for the US, the EU or Japan. While alternatives exist for the US and its allies, building an independent supply chain for gallium and germanium processing could require investment and could take years to develop as processing the elements can be costly, technologically complex, energy intensive and polluting42 .

Alternative sourcing countries include the US, Canada, Belgium and Germany for germanium, and South Korea and Japan for gallium. In addition, large stocks of government inventory are available in South Korea, which should soften the impact for the country's chipmakers. But ramping up production takes time due to the inability to process the materials, as well as existing environmental regulations that prevent processing and mining due to the significant pollution they cause. In the face of these challenges, the Democratic Republic of Congo may become a lifeline for Western countries as it may be able to contribute 30% of the world's germanium production with the development of a new plant43 .

The latest restrictions on China's exports of strategic minerals are not the first and will not be the last to be imposed internationally. Resource-rich countries on which the US and the Union depend for minerals are also adopting trade restrictions to require further downstream processing. These countries are seeking to expand the economic benefits of value-added processing, such as job creation and capital investment. For example, Indonesia, the world's largest nickel producer due to Chinese investment, banned the export of nickel ore in 202044 . Following Indonesia's model, the Philippines45 , the world's second largest producer of mined nickel, is considering banning or taxing the export of its nickel ore. Zimbabwe, which has Africa's largest lithium reserves and some of the world's largest hard rock lithium reserves, banned the export of unprocessed lithium in 202246 . Ghana and Namibia have also banned the export of unprocessed minerals47 . All these measures point to the fact that the supply chains of minerals needed for the energy and digital transition and also for the defence sector are highly vulnerable to possible restrictions48 .

Export controls also faced challenges that went beyond legal ones. The biggest problem facing the effectiveness of export control measures in the short term is smuggling. This had already been a problem before export controls; in 2009, smuggling accounted for 40% of China's rare earth exports, and at one point peaked at almost 50%49 .

Restrictions on mineral trade are also a consequence of protectionist measures that powers such as the US and the EU have put in place to counter their extreme vulnerability to a disruption of critical mineral supply chains.

On the one hand, the US, EU and Japan are seeking to minimise - if not eliminate - their dependence on China for both the extraction and processing of these critical minerals and are pursuing policy initiatives aimed at protecting domestic industry, seeking strategic alliances with new partners, diversifying sources of supply and seeking new extraction sites.

The EU Raw Materials Act - not yet passed - and the US Inflation Reduction Act (IRA) are examples of how policy is reshaping critical raw materials supply chains.

The IRA is part of Biden's Made in America policy agenda to address the high vulnerability of the US to supply chains for critical materials needed for the green and digital transition, affecting not only the energy sector but also the defence sector.

For the US, the IRA is a boost for the development of domestic industries related to clean energy. It sets out specific requirements to encourage domestic sourcing and manufacturing and provides tax incentives for companies that do final assembly in North America or in a country with which the US has a free trade agreement. The ultimate goal is to relocate supply chains for materials considered key to the energy and digital transition.

The IRA also explicitly targets inputs from so-called foreign entities of concern (China, Russia, North Korea or Iran) and stipulates that, from 2025, critical materials will no longer be allowed to come from any of these countries. At the moment, the US has only twenty free trade agreements, and only one with an African nation, Morocco, which could limit its ability to meet the growing demand for electric vehicles with an adequate supply of critical minerals50 .

For the US, the IRA is justified because it will allow the US to reduce greenhouse gas emissions by 37-41% in 2030 compared to 2005. But, in addition, with new national and/or federal regulatory measures these reductions could reach 50 %51 .

But there are indications that the scale of the IRA is already distorting the energy investment market, creating new uncertainties in a sector in transition52 . This suggests that climate policies are also contributing to the rise of domestic regulatory measures and increased protectionism that is reshaping global business transactions.

This more protectionist international trade environment could pose problems for companies dependent on foreign markets, especially in Europe and Asia53 .

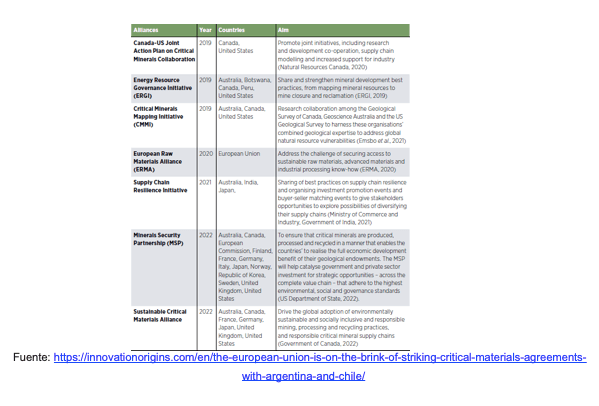

The rise of export restrictions and protectionism makes geostrategic alliances of like- minded countries increasingly important in a highly fragmented world. Proof of this is the US-Japan agreement54 , the possible EU agreement with the US55 , the future US agreement with India56 , the US action plan with Indonesia57 or the EU's proposed "critical raw materials club" which aims to source critical raw materials from "reliable partners who are willing to develop their own critical raw materials industries"58 .

Supply risks could be further amplified if some of the commodity-rich countries decide to form cartels. At present, it cannot be ruled out that some countries might create a commodity cartel similar to OPEC. Indeed, for example, Argentina, Chile and Bolivia, members of the lithium triangle, have been discussing this concept since July 202259 . Russia has also expressed the suitability of creating an OPEC-style platform for solid minerals60 .

The rise of nationalism is also a risk for critical mineral markets. For example, Bolivia has included the issue of lithium in the Constitution as a strategic resource61 , in Mexico, President López Obrador in 2022 declared Mexico's lithium deposits as national property by establishing a state-owned company, LithiumMx62 . In line with this trend, in 2023, policies to accelerate nationalisation have continued63 . In Chile, the ownership of the lithium industry is under discussion and the creation of a state-owned lithium company as already exists for copper is not ruled out64 . From a diplomatic point of view, some countries are establishing new alliances and partnerships to secure access to these critical mineral resources. As part of the EU Raw Materials Strategy, diplomacy has been prioritised, establishing strategic partnerships and political dialogues with third countries to secure access to raw materials on world markets.

Both the US and the EU are pursuing diplomatic initiatives to build better strategic partnerships in Africa to strengthen their supply chains. These are intended to dislodge China's deep presence from African territory. In contrast to China's purely extractive policies on the continent, the US and the EU offer a more attractive partnership model that aims to generate economic development in Africa's mineral-rich countries. In this way, Africa is becoming a crucial partner for the US and the EU in the geopolitical configuration of the 21st century65 .

Conclusions

As the world moves towards energy transition and technological progress, it is estimated that global demand for the critical minerals needed for these transformations may in- crease by 400-600 % or more in the coming decades.

The high concentration of production and processing of these minerals is an extreme vulnerability for powers dependent on external supplies such as the US, the EU and Japan.

Fragmentation of supply chains together with the rise of national and regional protectio- nist measures are some of the risks to the critical minerals economy.

China, the world's leading producer and export source of many of these minerals, has already shown its willingness to impose export controls on national security grounds. Un- der cover of this justification, geopolitical tension between China and the US is distorting the market for these resources, which is increasingly less driven by economics and more by geopolitics.

All of this is creating a scenario that is contributing to what some experts have called geo- economic fragmentation. In this context, the rise of export restrictions and protectionism make geostrategic alliances of like-minded countries increasingly important in an increa- singly fragmented world.

Mar Hidalgo García

IEEE Analyst @ieee_mhidalgo

References:

Note: All hyperlinks are active as of 12 February 2024.

1 https://www.whitehouse.gov/briefing-room/statements-releases/2022/02/22/fact-sheet-securing-a-made-in-america- supply-chain-for-critical-minerals/

2 https://www.iea.org/news/clean-energy-demand-for-critical-minerals-set-to-soar-as-the-world-pursues-net-zero- goals

3 https://ec.europa.eu/docsroom/documents/42881

4 https://www.whitehouse.gov/briefing-room/statements-releases/2022/02/22/fact-sheet-securing-a-made-in-america- supply-chain-for-critical-minerals/

5 https://www.imf.org/en/Publications/WP/Issues/2023/09/28/Geoeconomic-Fragmentation-and-Commodity-Markets-

539614

6 https://www.imf.org/en/Blogs/Articles/2023/08/28/the-high-cost-of-global-economic-fragmentation

7 IRENA. Geopolitics of the energy transition: Critical materials, International Renewable Energy Agency. Abu Dhabi, 2023.

8 https://www.foreignaffairs.com/world/price-fragmentation-global-economy-shock

9 Ibíd.

10 https://www.imf.org/es/News/Articles/2023/03/30/sp032923-md-boao-forum-remarks

11 AIYAR, Shekhar, ILYINA, Anna, and others. Geoeconomic Fragmentation and the Future of Multilateralism. Staff Discussion Note SDN/2023/001. International Monetary Fund, 2023.

12 https://www.review-energy.com/otras-fuentes/la-ocde-advierte-que-las-restricciones-a-la-exportacion-de-materias- primas-pondrian-en-riesgo-la-transicion-verde

13 https://www.statista.com/statistics/1127203/critical-minerals-production-share-by-majority-producing-countries- global/

14 https://www.statista.com/statistics/603621/global-distribution-of-nickel-mine-production-by-select-country/

15 https://www.statista.com/statistics/677245/distribution-of-world-lithiuim-production-by-country/

16 https://www.esginvestor.net/a-game-of-geopolitical-strategy-critical-minerals/

17 https://georgetownsecuritystudiesreview.org/2023/06/01/chinas-monopoly-over-critical-minerals/

18 https://www.miteco.gob.es/content/dam/miteco/es/ministerio/planes-estrategias/materias-primas-minerales/hr- materias-primas-minerales_23-8-22_web_tcm30-544770.pdf

19 https://www.goldmansachs.com/intelligence/pages/resource-realism-the-geopolitics-of-critical-mineral-supply- chains.html

20 Informe disponible en: https://single-market-economy.ec.europa.eu/publications/study-critical-raw-materials-eu- 2023-final-report_en

21 https://www.foreignaffairs.com/world/price-fragmentation-global-economy-shock

22 Grafito sintético,incluidas las versiones de alta pureza, alta resistencia y alta densidad, así como para el grafitonatural en escamas . https://edition.cnn.com/2023/10/20/economy/china-graphite-export-curbs-hnk- intl/index.html

23 https://foreignpolicy.com/2023/07/06/china-tech-us-metal-export-yellen-gallium-germanium/

24 https://www.sciencedirect.com/science/article/pii/S0301420722003348

25 https://www.csis.org/analysis/de-risking-gallium-supply-chains-national-security-case-eroding-chinas-critical- mineral

26 https://investornews.com/critical-minerals-rare-earths/china-selects-critical-mineral-gallium-as-weapon-of-choice/

27 https://investornews.com/critical-minerals-rare-earths/china-selects-critical-mineral-gallium-as-weapon-of-choice/

28 https://www.lazard.com/research-insights/critical-materials-geopolitics-interdependence-and-strategic-competition/

29 https://www.siliconexpert.com/blog/chinas-restricts-gallium-and-germanium/

30 Sustainability 7, 11818-11837, 2015, doi:10.3390/su70911818.

31 https://www.statista.com/statistics/1062116/global-germanium-production-by-country/

32 Disponible en: https://www.crmalliance.eu/germanium#:~:text=Where%20is%20Germanium%20Produced%3F&text=The%20major

%20worldwide%20producer%20of,Russia%20and%20the%20United%20States

33 https://africa.businessinsider.com/local/markets/congo-sees-opportunity-as-chinese-export-limits-on-gallium-and- germanium-raise-global/556f7wq

34 https://www.csis.org/analysis/chinas-use-graphite-export-restrictions-encourages-diversification

35 «El programa de fusión militar-civil integra los esfuerzos de planificación en innovación tecnológica militar con el desarrollo de infraestructuras, logística y capacidades industriales, para permitir a China adaptarse con rapidez a una contingencia bélica». Extraído de CE China: el desafío de la nueva potencia global, p. 22. Disponible en: https://www.ieee.es/publicaciones-new/cuadernos-de-estrategia/2022/Cuaderno_212.html

36 https://www.stimson.org/2023/why-chinas-export-controls-on-germanium-and-gallium-may-not-be- effective/ps://www.imf.org/en/Publications/fandd/issues/2023/06/challenge-of-export-controls-chad-bown

37 https://www.fastmarkets.com/insights/china-restrictions-on-gallium-germanium-harmful-us-chipmakers/

38 https://www.xataka.com/empresas-y-economia/china-consuma-su-golpe-maestro-eeuu-agosto-se-registraron-cero- exportaciones-galio-germanio

39 https://www.nasdaq.com/articles/chinas-oct-germanium-exports-rise-but-export-restrictions-limit-gains

40 https://www.wto.org/english/res_e/publications_e/wtr10_oecd2_e.htm

41 https://www.noemamag.com/china-wants-to-ditch-the-dollar/

42 https://edition.cnn.com/2023/10/11/tech/china-chips-gallium-germanium-intl-hnk/index.html

43 https://www.miningweekly.com/article/congo-eyes-30-of-germaniums-global-output-by-tapping-new-plant-2023-10-06

44 https://asia.nikkei.com/Spotlight/Caixin/Chinese-nickel-miners-in-Indonesia-face-threat-from-falling-prices

45 https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/philippines-seeks-to-follow-in- indonesia-s-footsteps-with-nickel-export-ban-74109353

46 https://www.globaltradealert.org/state-act/71304/zimbabwe-export-ban-on-unprocessed-lithium

47 https://www.downtoearth.org.in/news/africa/green-minerals-race-ghana-approves-policy-to-reap-maximum- benefits-from-mining-projects-91096

48 https://mwi.westpoint.edu/what-if-americas-mineral-intensive-military-runs-out-of-minerals/

49 https://www.stimson.org/2023/why-chinas-export-controls-on-germanium-and-gallium-may-not-be-effective/

50 https://www.energymonitor.ai/sectors/power/the-countries-controlling-the-critical-minerals-supply-chain-in-four- charts/?cf-view

51 Como la Ley de Reducción de la Inflación…-pdf

52 Ibíd.

53 https://www.bradley.com/insights/publications/2023/07/impacts-of-the-inflation-reduction-act-one-year-on

54 https://ustr.gov/about-us/policy-offices/press-office/press-releases/2023/march/united-states-and-japan-sign- critical-minerals-agreement

55 https://www.europarl.europa.eu/thinktank/en/document/EPRS_BRI(2023)754617

56 https://ustr.gov/about-us/policy-offices/press-office/press-releases/2024/january/joint-statement-united-states-india- trade-policy-forum

57 https://id.usembassy.gov/joint-statement-from-the-leaders-of-the-united-states-and-the-republic-of-indonesia- elevating-relations-to-a-comprehensive-strategic- partnership/#:~:text=The%20United%20States%20and%20Indonesia%20intend%20to%20pursue%20an%20ambiti 58 https://ec.europa.eu/commission/presscorner/detail/en/ip_23_1661

59 https://www.mining-technology.com/features/will-the-lithium-triangle-form-the-new-opec/?cf-view

60 https://tass.com/russia/1730257

61 https://cenital.com/el-triangulo-del-litio/

62 https://elpais.com/mexico/2023-02-18/lopez-obrador-promete-en-sonora-el-litio-para-todos-los-mexicanos.html

63 https://www.dof.gob.mx/nota_detalle.php?codigo=5662345&fecha=23/08/2022

64 https://www.eleconomista.es/mercados-cotizaciones/noticias/12239402/04/23/chile-nacionalizara-el-litio-una- ambicion-de-convertirse-en-el-centro-minero-de-la-codiciada-materia- prima.html#:~:text=Chile%20nacionalizar%C3%A1%20el%20litio%20para%20intentar%20c

65 https://www.atlanticcouncil.org/blogs/new-atlanticist/how-the-us-can-build-better-strategic-partnerships-in-africa-to- secure-critical-minerals/